To share or not to share…

Wow! Now that we are almost half a month into 2020, I thought I’d write a series of recaps from 2019. I am not yet comfortable sharing net worth numbers (unlike my wife who blurted it out to her very rich uncle one inebriated night), but I wanted to showcase our growth over last year.

So what is net worth? Simply, it is your total assets minus your liabilities. How much you have minus what you owe.

Assets

There are arguments that involve what to include as part of your assets. Vicki Robin wrote in her book, Your Money or Your Life, that everything you own should be included as part of your assets. Take a look around your house, you probably have a lot of stuff that was worth a lot of money at some point. The Motley Fool website also suggests including home furnishings, art, and jewelry into your net worth calculation in their article on How to Calculate your Net Worth.

I take an approach that is closer to frugality-cult creator, Mister Money Mustache (MMM) and exclude stuff like your car, furniture, and electronic devices. I mean, our $400 ottoman has suffered through years of cat puke, cat hair, and humans and isn’t worth squat to anyone. MMM outlines assets in his article, How Rich are You?, as all properties owned, and any monies in 401(k)s, IRAs, bank accounts, etc.,

Now if you have a Picasso then A) you are probably not reading my blog and B) you already know your net worth or have someone figuring it out for you! In other words, if you have an asset of some sort that is of high value and you know you can obtain the cash equivalent, then yes include it in your total asset value. I, for example, am leaving off my HeroClix collection despite shelling out tons of money for them back in the day.

The only things we include as our assets are our cash sitting in our various accounts and our properties. Our cash make up consists of monies in our HSA account, Traditional and Roth IRAs, 401(k)/403(b)s, and various ETFs and individual stocks. Our properties are two investment condos we own in Chicago. This value of our property is tricky in that we have not had either appraised since we purchased them. No way we are basing their value from Redfin or Zestimate so we’ve simply left the worth from the last appraisal. If we decide to get another appraisal, then we will update the number.

Liabilities

Liabilities are easy. Basically, if you owe someone something, then it is a liability. Examples include the amount left on your car, mortgages, any balance on your credit cards, student loans, and money you owe to your Uncle Bob (unless of course, you listen to Leo).

In case you missed this earlier post, we paid off our student loans this year! So, for us in 2019 our liabilities were credit card balances (we always pay these off every month, but that is another post), student loans for three quarters of the year, and our two mortgages.

Assets minus Liabilities

So there you go, add up all your assets, subtract out your liabilities. There are many ways you can do this math for yourself, but there are also many websites that allow you to plug in your information to calculate it for you. Personal Capital and Mint are cash tracking companies that will evaluate your net worth continuously. AARP and Chris Hogan have calculators for their members. Pro-tip: you need not be retired or a senior to join AARP!

But seriously, you don’t need to join and pay money to calculate your net worth. Nerd Wallet provides you with the template you need to do this in Excel, which is what I do. Excel allows me to create reports and geek out on the numbers. I save it to the cloud and look at it often, especially when I’m not feeling like working, and realize we’re getting closer to our financial goals.

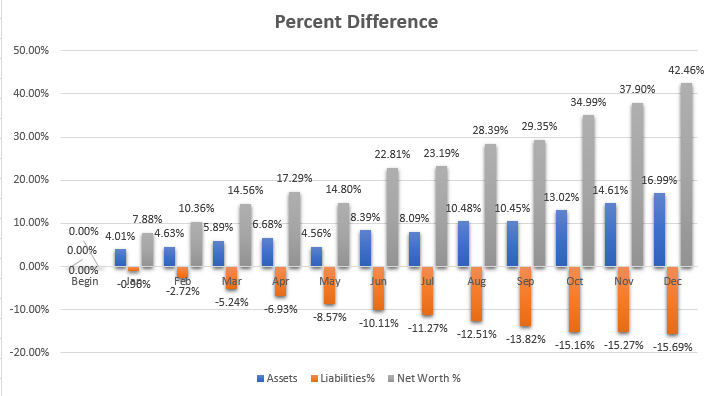

Bottom line, I do recommend that you get intimate with your money. People like Grant Sabatier at Millennial Money have influenced me in becoming more aware of our money. I spend about 2 hours each month calculating and tracking it. This has become a very cathartic hobby for me. By doing it myself, on Excel, I am able to create reports, like the one below, which shows our net worth percent increase for the year.

As the graph shows, we increased our net worth 42.46% last year! We were able to drop our liabilities by 15.69%, which was mainly our student loans. Our assets, which again included our monies and our stagnant home values, only increased 16.99%. Which heck, if we can increase our assets more than decreasing our liabilities while at the same time nearly half increasing our net worth, I’d say it was a good year.

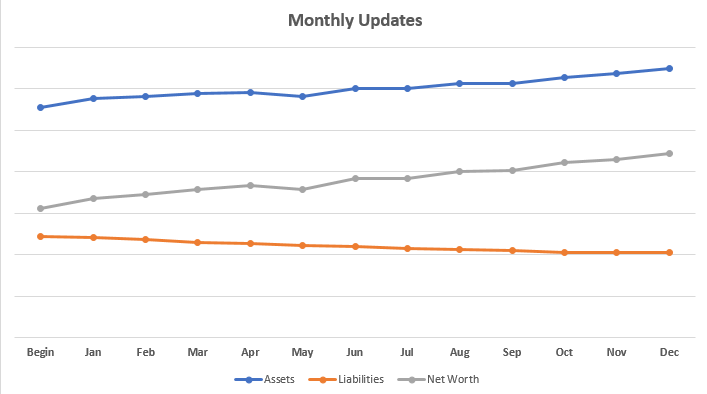

Here is a linear graph of our increase, just cause we can show it. Again, from the power of Excel – once you get beyond being a little scared of the tool. In all likelihood, you probably have Excel on your computer or access to it (check the library), and I think it is way more robust and easier to use than any of the sign ups I posted above for what you need (ask me for help!).

Why calculate your net worth?

Who cares right? Well you should. You should at least be comparing yourself to yourself (and no one else really) to see if you are moving towards your goals. You simply don’t know what you don’t know, and if you don’t know your net worth, how do you know if you are moving towards what you desire?

If you want me to help you figure out your net worth, please reach out. I love doing this kind of thing and can help you interpret the results. Similar to Ramit Sethi, in his post at I will teach you to be rich, I can show you ways on increasing and protecting your net worth. Dave Ramsey is a more popular figure in the wealth space, and I’m pretty well versed on his teachings as well. While I do not agree 100% with his philosophy, some of his teachings, such as What is Your Net Worth article, are important to know. Do not let net worth scare you, every one is in a different position, based on needs and goals.

Look at these numbers

Here are some examples of what I mean by everyone is in a different place. Big ERN at Early Retirement Now, posts his net worth. He is sitting, or was back in 2018, at a net worth of $3.4 million! He only recently retired in 2019. However, A Purple Life, posted her 2019 net worth at $448,230 and is setting her sight to retire later this year at the age of 30. So everyone has different goals, different numbers, etc. I would not put too much faith in articles that tell you that you need to have a net worth of X by age Z. They have no idea where you live, what you do, or how much money you need! Only you know that, or should know that, and if you like, I can help with that!