Happy Halloween! I nicked this meme from the RN to Wealthy Facebook feed, but the point is clear. Student loans have become a scary thing faced by many Americans. According to the federal reserve, in their Report of Economic Well-Being of Households in 2016, 30% of American’s have taken out some form of a loan to pay for continuing education. Per the Federal Reserve Bank in New York, of $13.51 trillion dollars of the total debt balance in the US in Q3 of 2018, 11% of it was from student loans. That is a total of $1.56 trillion across 44.7 million Americans!

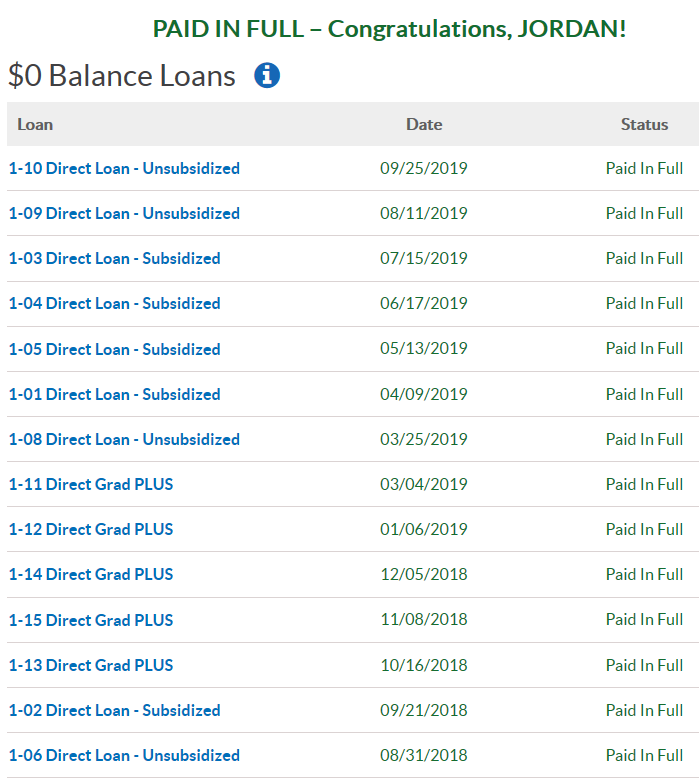

As of today, I am proud to say, that we are no longer part of that statistic!

Happy Day

Sadly we didn’t submit our last payment with a Champagne toast, or even go out and celebrate, we just clicked on the payment option. Navient didn’t really seem to care either, not even a balloon release nor confetti toss gif. But for us, this means freedom from forking over $1,400 a week to pay down these loans.

Yes, you read that right! When Jordan and I decided to be serious in tackling our student loans, we committed some serious money towards our payments.

How it started

Our love story will have to wait until another day, but before we met each other, neither of us had any student loan debt. But by the time we said our nuptials and committed our lives and baggage to each other, we had accumulated over $140,000 in student loans. Jordan with a Doctorate in Physical Therapy and me with a Bachelor of Science in Nursing (this was my second Bachelors too).

I had about $20k in private loans with interest rates out the wazoo, but Jordan’s was a federal student loan with low interest. We quickly paid off mine and settled into the norm of making minimal payments for the life of the loan, or at least for the 20 years until they went away. Yes, this was a big mistake but we had just gotten married and we were buying a condo so we only committed to the minimum payments towards repaying these loans – life of a pre-FI’er.

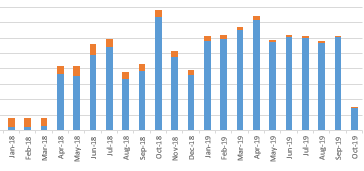

Here is the timeline of our total payments made:

Kind of difficult to see, click to expand. Around November 2013 we adjusted our payments so the minimum was even lower! In the graph above, the blue line represents the principle payment, orange interest payment, and gray total payment. You can see that for a span of time, we were really making little head way on the principle but were paying a lot in interest. Here is a stacked graph of the timeline from February 2014 to March 2018, the coast period, or the time we were sleeping our way through our payments:

This is insane! Again blue is the payment towards principle, orange is the interest payment. For about 4 years, our average monthly payment towards the principle was $197 while our average monthly payment towards interest was $610!

The graph shows our balance over time:

As you can (again, difficult to) see, there is a STEEP decline. In March 2018, we decided enough of these damn student loans and put more money into it. Looking back to the first graph, the Navient Payments graph, you’ll notice this by the steep incline in the payments starting April 2018. Below is the stacked bar chart when we decided to pay more on the interest:

Again, orange is interest, blue is principle. Our principle payment jumped to $4,900 a month for 20 months and our average interest payment dropped to $331 a month! This was nuts to us when we first looked at this graph!

If more people would take a look, proactively, at what they are paying and compare it to what they could be paying, it could save them so much more in the long run. I wish we wouldn’t have had our “idle” or “coast” time as long as we did just casually making low payments. I can’t even imagine how much we could have saved.

After some work, we are no longer a student loan statistic. We can now steer the $4,900 a month towards other things such as long term investments or paying off one of our condos – yeah, that again is another story.

What about you? Have you taken the time to look at what you are paying? Have you mapped out different payment options? For a time, I was making payments daily! That was an experiment I did for a month to see if it would drop my interests (spoiler alert – it didn’t). Do you need help mapping something like this out? I would love to help you! I mean, I may have some free time now that I no longer have to chart out our student loans!